YV Reddy, the former governor of Reserve Bank of India (RBI), once lamented that global financial conglomerates are "larger and, perhaps, more powerful than some of the central banks."

Today, that may not necessarily be the case and the possibility of these banks becoming a dominant force in the Indian banking space seems to have faded. Global banks have surely gotten big in India — over the last 15 years, the total advances of foreign banks in India have doubled every five years from Rs 75,318 crore in March 2005 to Rs 1.63 lakh crore in 2010 and to Rs 3.27 lakh crore in March 2015.

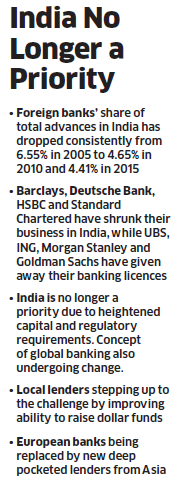

But that's just half the story. The real story is the slow but sure slide of foreign banks' market share. From 6.55% in 2005, foreign banks' share of advances dropped to 4.65% in 2010 and to 4.41% in 2015. In January, the UK-based Barclays shut down its equity capital market and broking business in India, continuing a trend of full or part exit of foreign banks since 2009.

In the last five years, Deutsche Bank has sold its credit card business, Barclays has shut its retail banking business; Swiss lender UBS has given up its banking licence and so did US-based multinationals Morgan Stanley and Goldman Sachs; Bank of America-Merrill Lynch sold its wealth management business to Julius Baer and Dutch banking group ING sold its Indian operations to homegrown Kotak Mahindra Bank.

The exodus continued in 2015 with British bank RBS, which in 2013 shut 23 of its 31 branches in India, saying it will no longer continue in the country. Late last year, Standard Chartered reduced by a quarter its staff in corporate and investment banking. HSBC, too, said it will shut down its private banking business.

The trend is clear. A fast-growing India has ceased to be a priority for multinational foreign banks since the financial crisis, as high capital and regulatory requirements at home have forced them to retreat into their domestic markets to save on costs and protect profitability. Bankers say this pullout from India is an indication of the demise of global banking as we knew it at the turn of the century.

"Big is not beautiful anymore in banking. People can tell me whatever they want but this global, anywhere, anytime model for banking is not possible or valuable anymore," Boris Collardi, CEO at Swiss private bank Julius Baer, told ET in an interview. Collardi said his bank saw the signs of this change early and shed it asset management, corporate investment bank businesses to focus solely on wealth management in the last 15 years because "we believe we can only be outstanding in one thing."

Tectonic shift

Indian bankers echo their global counterparts. Global banking, they say, is no longer practical. "There has been a tectonic shift in global banking post the crisis. Big, bulge-bracket banks have had to remodel themselves.

The diminishing return of large global banks does not justify their presence in India. The banking model has changed to a home country one," Rana Kapoor, MD at Yes Bank who spent 23 of his 36-year career at foreign banks, said. It's now back to basic banking. Higher capital requirements post Lehman Brothers' demise, intervening regulations for different geographies and pressure from governments to conserve capital in home markets have forced banks to be less ambitious.

RBS, for example, had to seek a £46-billion bailout from the British government post September 2008. "Speculative trading products and client advisory have become more expensive. Regulators have become tough. RBS, for example, went from one crisis to another after the government bailout — from the LIBOR fixing scandal to a mortgage scandal and a mis-selling scandal in the UK.

RBS, for example, had to seek a £46-billion bailout from the British government post September 2008. "Speculative trading products and client advisory have become more expensive. Regulators have become tough. RBS, for example, went from one crisis to another after the government bailout — from the LIBOR fixing scandal to a mortgage scandal and a mis-selling scandal in the UK.

Everything has resulted in fines and higher costs, exploding the cost-to-income ratio," said a senior executive from the bank, explaining why it had to exit emerging markets like India. Collardi calls the capital requirements and regulatory "overhang" for different businesses "unbearable," joking that some of his counterparts who manage much bigger banks elsewhere across the globe have to deal with as many as 500 differently regulated activities worldwide.

"The cost of complexity of running a big bank today is also correlated to the number of regulators you need to respond to. Now, we have a lot of conflicting regulations. Everybody wants their bank to be locally capitalised, so we are getting into a new paradigm," he said. In fact, their dwindling power seems to have resulted in the RBI putting on back burner its plans to make foreign banks subsidiarise and list on the Indian stock exchanges.

Enduring turmoil

The recent volatility in global markets has thrown up some interesting comparisons as Indian private sector banks are being valued higher than their more-famed global counterparts.

In February, HDFC Bank, India's second-largest private lender by assets and the second-most expensive bank globally, overtook European banks like Deutsche, Credit Suisse and Societe Generale in market capitalisation. The market capitalisation of Kotak Mahindra Bank, with just 1% of Deutsche Bank's assets, was only $1 billion less than the German lender's; the difference was $24 billion a year ago.

India is the only country outside Europe where the German lender has retail banking presence, fuelling speculation it would discontinue these operations soon. However, in an interview earlier this month, Deutsche Bank's Asia Pacific CEO Gunit Chadha said there are no plans to shrink the Indian business. "Deutsche Bank India sale was never ever on the table....the global banking industry must reinvent its business models.

We ourselves have some challenges, which we are proactively addressing, but our commitment to Asia Pacific is strong and stays fully intact," Chadha said in the interview. Deutsche Bank has 17 branches in India currently with a Rs 5,000 crore mortgage book and `15,000 crore in wealth management. Last year, it sold its mutual fund business to Pramerica Mutual Fund.

US banks are also not immune. In December 2015, USbased Citibank was widely reported to be cutting up to 2,000 jobs globally as it continues to restructure its business and exit markets too small to be meaningful for its business. It has already wound down its non- banking finance company in India in 2009.

The Opportunity

Private sector bankers say foreign banks are exiting India because of their own problems. "These banks had profitable businesses here providing crossborder linkages and dollar funding to Indian clients.

These linkages still exist and foreign banks still have a lot to offer in terms of transaction products for companies," said Romesh Sobti, MD at IndusInd Bank. Sobti believes there are many foreign lenders waiting to enter India and fill the gap left by these European banks.

One such lender, National Bank of Abu Dhabi (NBAD), started operations in October 2015 with an aggressive intent by buying $1 billion of Indian external commercial borrowings (ECBs) from The Royal Bank of Scotland (RBS). "We have strong capital and ratings position, relationship with Indian clients and have identified India as an important market. We have a clear strategy to grow in India," said Rajeev Pant, regional CEO, South Asia, at NBAD.

Indian private sector lenders are also ready to fill in the space vacated by the foreign lenders. Banks like Yes Bank, IndusInd Bank and Kotak Mahindra Bank, which do not have any overseas branch, will open units in the Gujarat International Finance Tec-City (GIFT), with the prospect of raising dollar-denominated funds, which were once the sole monopoly of foreign banks in India. "Through the financial centre, we can raise dollar funds.

We also have global alliances with more than 900 banks. We believe alliances, relationships and technology will be important in banking from here on," Kapoor of Yes Bank said. In the first few weeks of 2016, shares of global banks, including Deutsche, Standard Chartered,HSBC and even Wells Fargo, fell between 12% and 40% as investors questioned whether these banks have enough capital to support growth. The banks once seen as gorillas may be becoming pygmies, at least in India.

Today, that may not necessarily be the case and the possibility of these banks becoming a dominant force in the Indian banking space seems to have faded. Global banks have surely gotten big in India — over the last 15 years, the total advances of foreign banks in India have doubled every five years from Rs 75,318 crore in March 2005 to Rs 1.63 lakh crore in 2010 and to Rs 3.27 lakh crore in March 2015.

But that's just half the story. The real story is the slow but sure slide of foreign banks' market share. From 6.55% in 2005, foreign banks' share of advances dropped to 4.65% in 2010 and to 4.41% in 2015. In January, the UK-based Barclays shut down its equity capital market and broking business in India, continuing a trend of full or part exit of foreign banks since 2009.

In the last five years, Deutsche Bank has sold its credit card business, Barclays has shut its retail banking business; Swiss lender UBS has given up its banking licence and so did US-based multinationals Morgan Stanley and Goldman Sachs; Bank of America-Merrill Lynch sold its wealth management business to Julius Baer and Dutch banking group ING sold its Indian operations to homegrown Kotak Mahindra Bank.

The exodus continued in 2015 with British bank RBS, which in 2013 shut 23 of its 31 branches in India, saying it will no longer continue in the country. Late last year, Standard Chartered reduced by a quarter its staff in corporate and investment banking. HSBC, too, said it will shut down its private banking business.

The trend is clear. A fast-growing India has ceased to be a priority for multinational foreign banks since the financial crisis, as high capital and regulatory requirements at home have forced them to retreat into their domestic markets to save on costs and protect profitability. Bankers say this pullout from India is an indication of the demise of global banking as we knew it at the turn of the century.

"Big is not beautiful anymore in banking. People can tell me whatever they want but this global, anywhere, anytime model for banking is not possible or valuable anymore," Boris Collardi, CEO at Swiss private bank Julius Baer, told ET in an interview. Collardi said his bank saw the signs of this change early and shed it asset management, corporate investment bank businesses to focus solely on wealth management in the last 15 years because "we believe we can only be outstanding in one thing."

Tectonic shift

Indian bankers echo their global counterparts. Global banking, they say, is no longer practical. "There has been a tectonic shift in global banking post the crisis. Big, bulge-bracket banks have had to remodel themselves.

The diminishing return of large global banks does not justify their presence in India. The banking model has changed to a home country one," Rana Kapoor, MD at Yes Bank who spent 23 of his 36-year career at foreign banks, said. It's now back to basic banking. Higher capital requirements post Lehman Brothers' demise, intervening regulations for different geographies and pressure from governments to conserve capital in home markets have forced banks to be less ambitious.

RBS, for example, had to seek a £46-billion bailout from the British government post September 2008. "Speculative trading products and client advisory have become more expensive. Regulators have become tough. RBS, for example, went from one crisis to another after the government bailout — from the LIBOR fixing scandal to a mortgage scandal and a mis-selling scandal in the UK.Everything has resulted in fines and higher costs, exploding the cost-to-income ratio," said a senior executive from the bank, explaining why it had to exit emerging markets like India. Collardi calls the capital requirements and regulatory "overhang" for different businesses "unbearable," joking that some of his counterparts who manage much bigger banks elsewhere across the globe have to deal with as many as 500 differently regulated activities worldwide.

"The cost of complexity of running a big bank today is also correlated to the number of regulators you need to respond to. Now, we have a lot of conflicting regulations. Everybody wants their bank to be locally capitalised, so we are getting into a new paradigm," he said. In fact, their dwindling power seems to have resulted in the RBI putting on back burner its plans to make foreign banks subsidiarise and list on the Indian stock exchanges.

Enduring turmoil

The recent volatility in global markets has thrown up some interesting comparisons as Indian private sector banks are being valued higher than their more-famed global counterparts.

In February, HDFC Bank, India's second-largest private lender by assets and the second-most expensive bank globally, overtook European banks like Deutsche, Credit Suisse and Societe Generale in market capitalisation. The market capitalisation of Kotak Mahindra Bank, with just 1% of Deutsche Bank's assets, was only $1 billion less than the German lender's; the difference was $24 billion a year ago.

India is the only country outside Europe where the German lender has retail banking presence, fuelling speculation it would discontinue these operations soon. However, in an interview earlier this month, Deutsche Bank's Asia Pacific CEO Gunit Chadha said there are no plans to shrink the Indian business. "Deutsche Bank India sale was never ever on the table....the global banking industry must reinvent its business models.

We ourselves have some challenges, which we are proactively addressing, but our commitment to Asia Pacific is strong and stays fully intact," Chadha said in the interview. Deutsche Bank has 17 branches in India currently with a Rs 5,000 crore mortgage book and `15,000 crore in wealth management. Last year, it sold its mutual fund business to Pramerica Mutual Fund.

US banks are also not immune. In December 2015, USbased Citibank was widely reported to be cutting up to 2,000 jobs globally as it continues to restructure its business and exit markets too small to be meaningful for its business. It has already wound down its non- banking finance company in India in 2009.

The Opportunity

Private sector bankers say foreign banks are exiting India because of their own problems. "These banks had profitable businesses here providing crossborder linkages and dollar funding to Indian clients.

These linkages still exist and foreign banks still have a lot to offer in terms of transaction products for companies," said Romesh Sobti, MD at IndusInd Bank. Sobti believes there are many foreign lenders waiting to enter India and fill the gap left by these European banks.

One such lender, National Bank of Abu Dhabi (NBAD), started operations in October 2015 with an aggressive intent by buying $1 billion of Indian external commercial borrowings (ECBs) from The Royal Bank of Scotland (RBS). "We have strong capital and ratings position, relationship with Indian clients and have identified India as an important market. We have a clear strategy to grow in India," said Rajeev Pant, regional CEO, South Asia, at NBAD.

Indian private sector lenders are also ready to fill in the space vacated by the foreign lenders. Banks like Yes Bank, IndusInd Bank and Kotak Mahindra Bank, which do not have any overseas branch, will open units in the Gujarat International Finance Tec-City (GIFT), with the prospect of raising dollar-denominated funds, which were once the sole monopoly of foreign banks in India. "Through the financial centre, we can raise dollar funds.

We also have global alliances with more than 900 banks. We believe alliances, relationships and technology will be important in banking from here on," Kapoor of Yes Bank said. In the first few weeks of 2016, shares of global banks, including Deutsche, Standard Chartered,HSBC and even Wells Fargo, fell between 12% and 40% as investors questioned whether these banks have enough capital to support growth. The banks once seen as gorillas may be becoming pygmies, at least in India.

No comments:

Post a Comment